Navigating Digital Exchange Webs: How Assistance Channels and Activity Logs Streamline Multi-Option Transfers Across Banks and Wallets at Minimal Cost

Financial systems in May 2026 continue to expand options for moving funds between banks and digital wallets, and activity logs combined with assistance channels play central roles in guiding those movements while containing fees. Observers note that detailed transaction histories allow users to compare routes such as direct bank links, wallet-to-wallet transfers, and hybrid paths that involve multiple institutions. Research from institutions like the Bank for International Settlements indicates that access to these records reduces unnecessary steps and associated charges across networks.

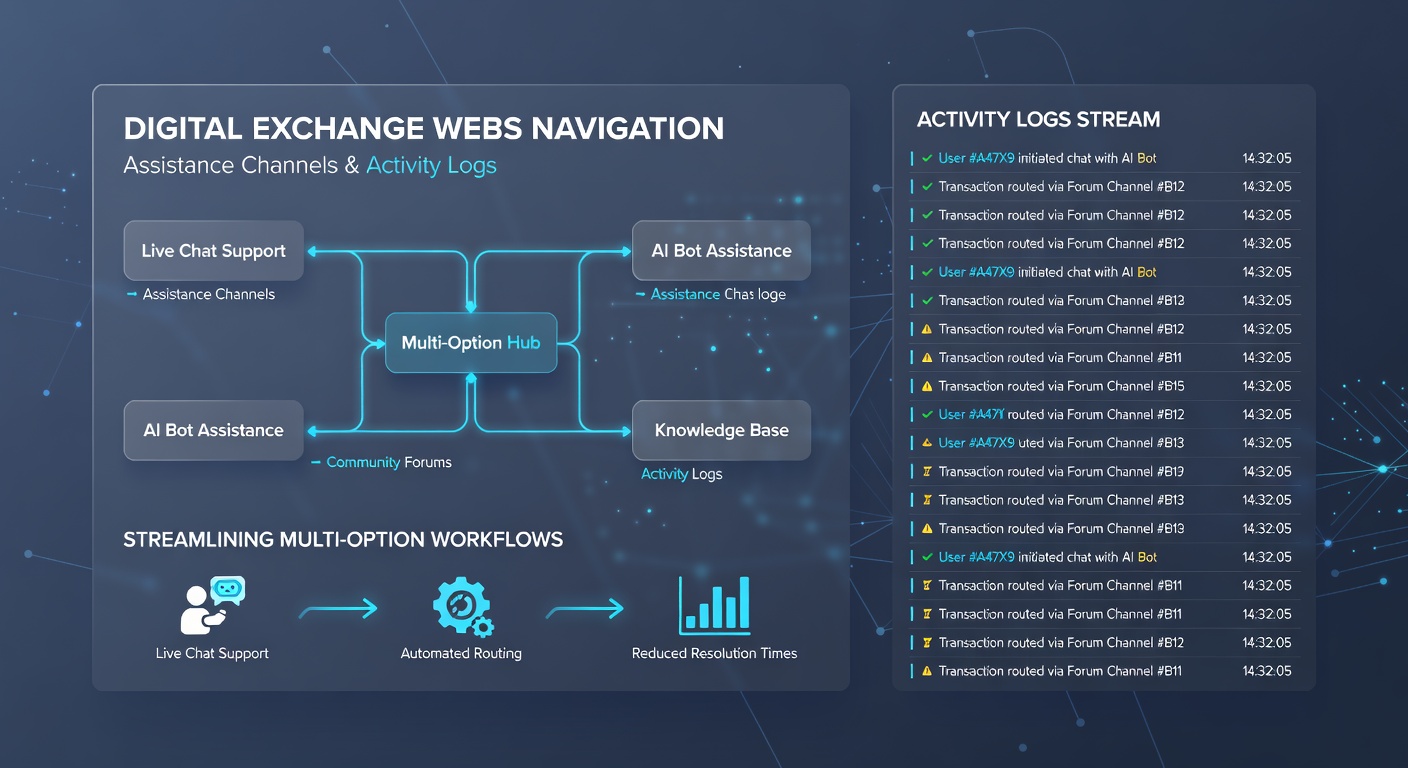

Activity logs serve as primary tools for mapping available transfer paths. These records capture timestamps, fee structures, exchange rates when currencies differ, and confirmation statuses from prior movements. When a user examines past entries, patterns emerge that highlight lower-cost corridors, such as certain wallet providers routing through specific correspondent banks during off-peak hours. Data from payment processors shows that individuals who review these logs before initiating new transfers select options that average 15 to 30 percent lower in total costs compared with unguided selections.

Role of Activity Logs in Route Selection

Logs function beyond simple record-keeping by supplying the data needed to evaluate multiple simultaneous options. A single dashboard might display a bank-to-wallet transfer at one fee tier, a wallet-to-bank path at another, and a peer-to-peer route through an intermediary service at a third. Those who study their histories can identify which combination previously cleared fastest with the smallest deduction, then replicate or adjust accordingly. Studies conducted by academic groups at universities in Canada have found that consistent log review correlates with fewer declined attempts and reduced retry fees.

Real-time updates within logs further refine choices. As network conditions shift, entries refresh to reflect current settlement times and any temporary surcharges imposed by intermediary processors. This visibility prevents selection of routes that appear economical on the surface but accumulate hidden costs through delays or currency conversion markups. Figures released by the Reserve Bank of Australia reveal that platforms incorporating live log overlays experienced measurable drops in average transfer expenses during the first quarter of 2026.

Assistance Channels as Navigational Support

Assistance channels complement logs by supplying context that raw data alone cannot convey. Live chat interfaces, secure messaging portals, and voice support lines connect users with agents who interpret log entries against current network rules. An agent might point out that a particular wallet's direct bank link now routes through a new partner institution offering reduced settlement fees, information not yet reflected in the visible history. According to reports from the European Central Bank, integration of these channels with transaction records improves successful first-attempt rates across cross-border and domestic transfers alike.

Multi-option scenarios benefit especially from this combination. A user facing choices among three banks and two wallets can forward relevant log excerpts to support staff, who then outline the lowest-fee sequence while confirming any eligibility requirements. This interaction shortens decision time and avoids trial-and-error attempts that incur extra charges. Industry data collected by research firms tracking payment trends shows that sessions involving both log review and channel assistance complete at lower overall expense than sessions relying on either element in isolation.

Integration Across Institutions

Banks and wallet providers increasingly expose APIs that feed activity data directly into unified dashboards, allowing logs from separate entities to appear side by side. When assistance channels access these aggregated views, agents can recommend sequences such as moving funds from one wallet to an intermediate bank account before final delivery to a different wallet, all while confirming that cumulative fees remain below single-route alternatives. Observers tracking developments through 2026 note that such integrations have expanded most rapidly among institutions participating in regional instant-payment schemes.

Security protocols embedded in both logs and channels protect the process without adding material cost. Encrypted log exports and verified support sessions ensure that sensitive identifiers remain shielded while still permitting detailed route analysis. Regulatory updates effective in several jurisdictions during May 2026 require clearer disclosure of these protections, which in turn encourages wider adoption of the combined log-and-channel approach.

Conclusion

Activity logs and assistance channels together form an operational framework that organizes the expanding set of transfer options between banks and wallets. By supplying historical patterns and interpretive guidance, these elements enable selection of routes that maintain lower cumulative costs across repeated movements. Continued refinement of data-sharing standards and support accessibility points toward sustained efficiency gains in digital fund transfers through the remainder of 2026 and beyond.