The Interplay of Confirmation Steps and User Histories in Facilitating Affordable Instant Access to Funds

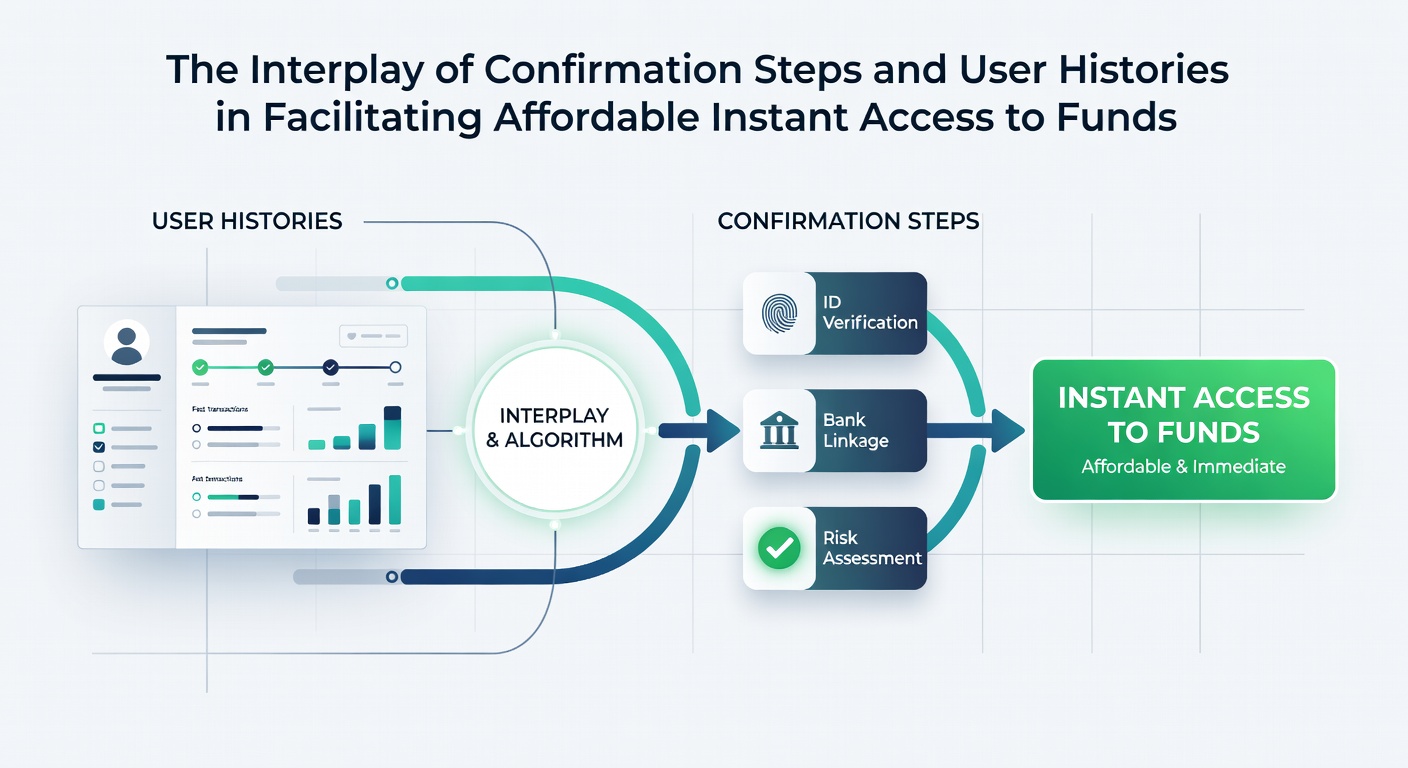

Financial systems around the world rely on confirmation steps paired with detailed user histories to balance speed, cost, and security in fund transfers. These elements work together in payment platforms, bank networks, and digital services where quick access matters most. In May 2026 observers note continued expansion of instant payment rails such as those operated by central banks, with transaction volumes rising steadily across multiple regions.

Confirmation Steps in Modern Payment Flows

Confirmation steps include identity checks, device verification, and transaction authorization prompts that platforms execute before releasing funds. Banks and fintech providers apply these measures at varying intensities depending on account details and transfer size. Layered confirmations such as one-time passcodes sent via mobile or biometric scans help reduce unauthorized activity while keeping most legitimate requests moving forward without delay.

Systems often adjust the number of required steps based on risk signals gathered in real time. A user attempting a small internal transfer might face only a single confirmation, whereas larger or cross-border movements trigger additional layers. Data from payment processors shows this adaptive approach maintains average processing times under ten seconds for qualifying transactions.

User Histories as Decision Inputs

User histories compile records of past transfers, login patterns, repayment behavior, and account tenure. Platforms store these details in secure databases that algorithms reference during each new request. Longer account histories with consistent activity patterns typically correlate with faster approvals and lower per-transaction fees.

Financial institutions examine frequency of successful transfers, average amounts, and geographic consistency to build risk profiles. Research from the Bank for International Settlements indicates that accounts with two or more years of clean history experience approval rates above 95 percent in automated instant systems. Shorter histories prompt manual reviews or extra confirmations that extend processing windows and sometimes add fees.

Combined Effects on Speed and Pricing

When confirmation steps integrate directly with user history data, platforms can skip redundant checks for established accounts. This integration reduces both operational costs and end-user charges. Automated scoring engines weigh history length against the current confirmation results, then route low-risk requests through priority channels that settle in seconds.

Take one regional bank that implemented combined scoring in 2024. Its records show average fees for instant domestic transfers dropped by 40 percent for accounts older than eighteen months, while processing times remained consistent across verified channels. Similar patterns appear in reports covering European instant payment schemes where history-based exemptions lowered overall system expenses.

Cross-border services apply the same principle by linking local confirmation records with international history feeds. Providers that maintain shared databases report fewer declined transactions and reduced chargeback rates, outcomes that translate into lower reserve requirements and ultimately cheaper access for users.

Technical Infrastructure Supporting the Interplay

Application programming interfaces connect confirmation engines with history repositories so decisions occur within milliseconds. Encryption protocols protect the data exchange, while audit logs track every access event for regulatory compliance. Cloud-based architectures allow scaling during peak periods without extending wait times for individual transfers.

Standards developed by industry groups encourage interoperability between banks and non-bank providers. These frameworks specify minimum data fields for history sharing and confirmation outcomes, enabling consistent experiences regardless of the originating service. Observers note that jurisdictions adopting such standards in 2025 recorded measurable gains in transaction throughput.

Regulatory Context and Data Handling

Regulators require platforms to document how they combine confirmation results with historical records. Guidelines from the Federal Reserve emphasize transparency in risk models while permitting automated decisions for low-value transfers. Canadian and Australian authorities apply comparable rules focused on consumer protection and data minimization.

Compliance teams review sample transactions monthly to verify that history-based shortcuts do not compromise security thresholds. Findings from these reviews feed back into model updates, refining the balance between speed and safeguards over successive iterations.

Conclusion

The interplay between confirmation steps and user histories continues to shape how financial services deliver affordable instant access. Platforms that align these components effectively achieve shorter processing windows and reduced fees while meeting security and compliance obligations. As payment networks evolve through 2026, ongoing refinements in data integration promise further efficiencies across domestic and international corridors.